Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

In recent news, there have been reports suggesting that renting may be a more affordable option compared to buying a home. While this might hold true in certain areas when considering monthly payments alone, there’s a crucial aspect that these reports often overlook: home equity. Let’s delve into the significance of equity and why it should factor into your decision-making process.

Basis of the Headlines

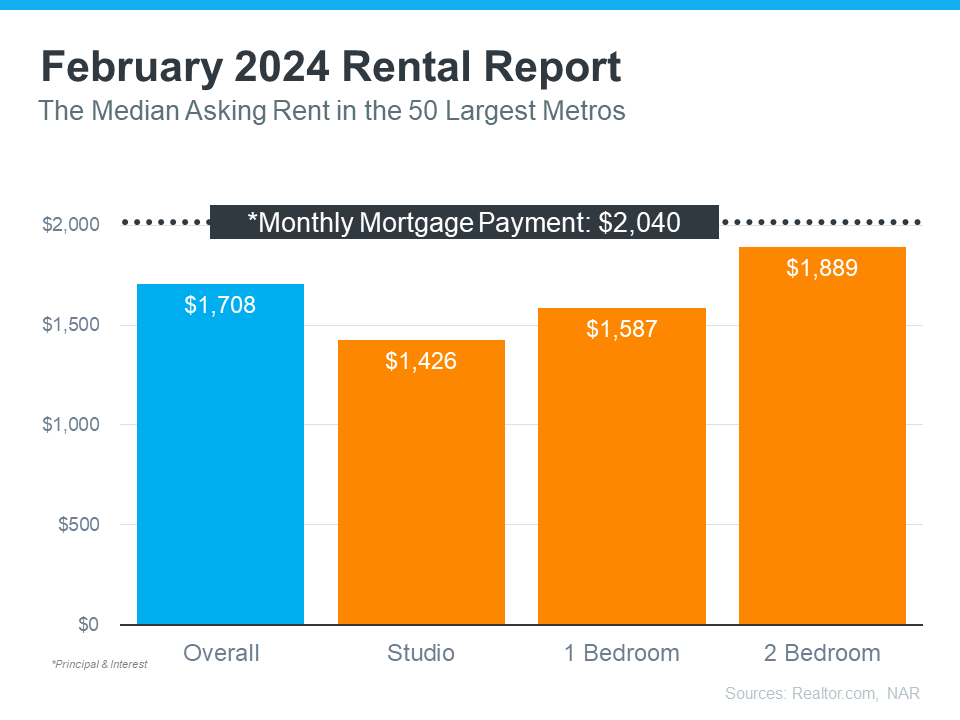

Utilizing national data on median rental payments from Realtor.com and median mortgage payments from the National Association of Realtors (NAR), comparisons between renting and buying can be made. The graph illustrates that particularly for those not requiring extensive space, renting may be more financially feasible on a monthly basis:

However, if you’re in the market for a property with two bedrooms, the disparity between median rent and median mortgage payments narrows, making the difference more manageable. The median monthly mortgage payment stands at $2,040, while the median monthly rent for two bedrooms is $1,889, reflecting a difference of approximately $151 a month. But, when equity is taken into account, the scenario changes significantly.

The Impact of Equity

When you opt to rent, your monthly payments solely cover your housing expenses and contribute to your landlord’s income. Essentially, apart from potentially saving a bit each month and receiving your rental deposit upon departure, the money spent on housing vanishes without any tangible return.

In contrast, purchasing a home not only covers your shelter through mortgage payments but also serves as an investment. With each mortgage payment, you incrementally build equity by reducing your outstanding home loan. Moreover, as property values typically appreciate over time, your equity receives an additional boost.

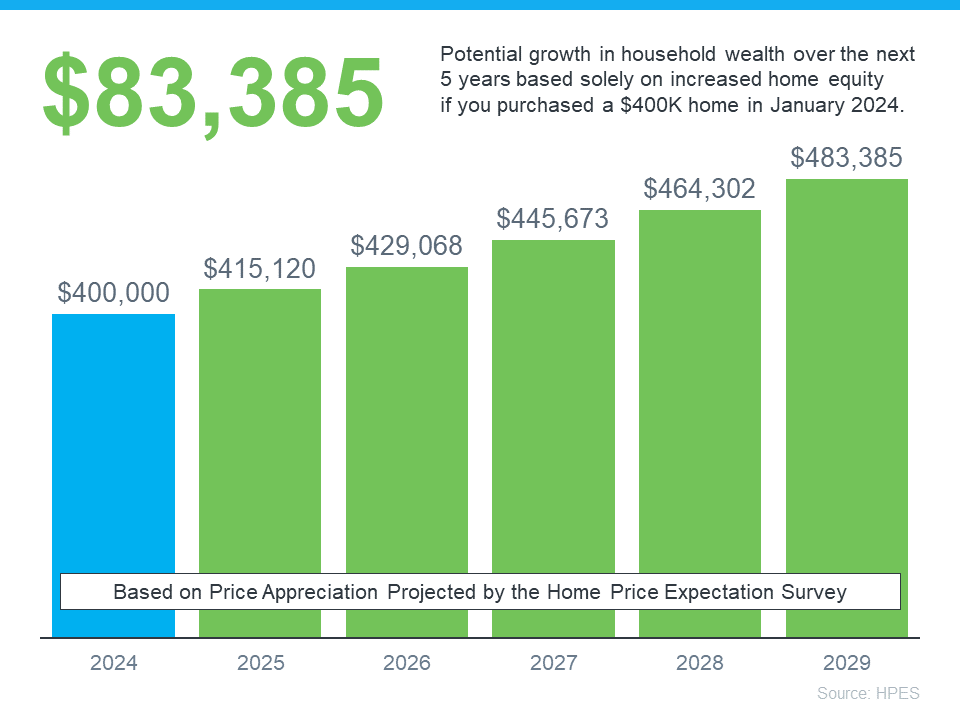

To grasp the substantial growth potential of equity, consider the data from the Home Price Expectations Survey (HPES) conducted quarterly by Fannie Mae and Pulsenomics. According to the latest projections, experts anticipate a continual increase in home prices over the next five years.

For instance, suppose you bought a home for $400,000 at the beginning of this year with the intention of residing there for an extended period. Based on HPES projections, after five years, you could potentially accumulate over $83,000 in household wealth as your home appreciates in value.

Comparing this wealth accumulation to renting, despite potential savings in monthly payments, renters miss out on the opportunity to gain equity.

In Conclusion

The decision of whether to rent or buy hinges on individual financial circumstances. It’s unwise to pursue homeownership if the financial aspects don’t align with your situation. However, for those financially prepared, recognizing equity as a crucial aspect may tip the scales in favor of buying in the long term.

Ultimately, buying a home offers a unique advantage that renting cannot match: the opportunity to build equity. If you’re interested in leveraging long-term home price appreciation, exploring your options for homeownership is worth considering.