Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Recent reports may have sparked concerns about a surge in foreclosures reminiscent of the 2008 housing crash. However, a closer examination of the data reveals a different story altogether.

The headlines may sound alarming, but the apparent increase in foreclosures is somewhat misleading. This is because the comparison is made against a period when foreclosures were unusually low due to measures like moratoriums and forbearance programs. As these measures have ended, it’s natural for foreclosure numbers to rise. Yet, this uptick is expected, not indicative of impending crisis. The rise in foreclosure filings does not signal trouble for the housing market.

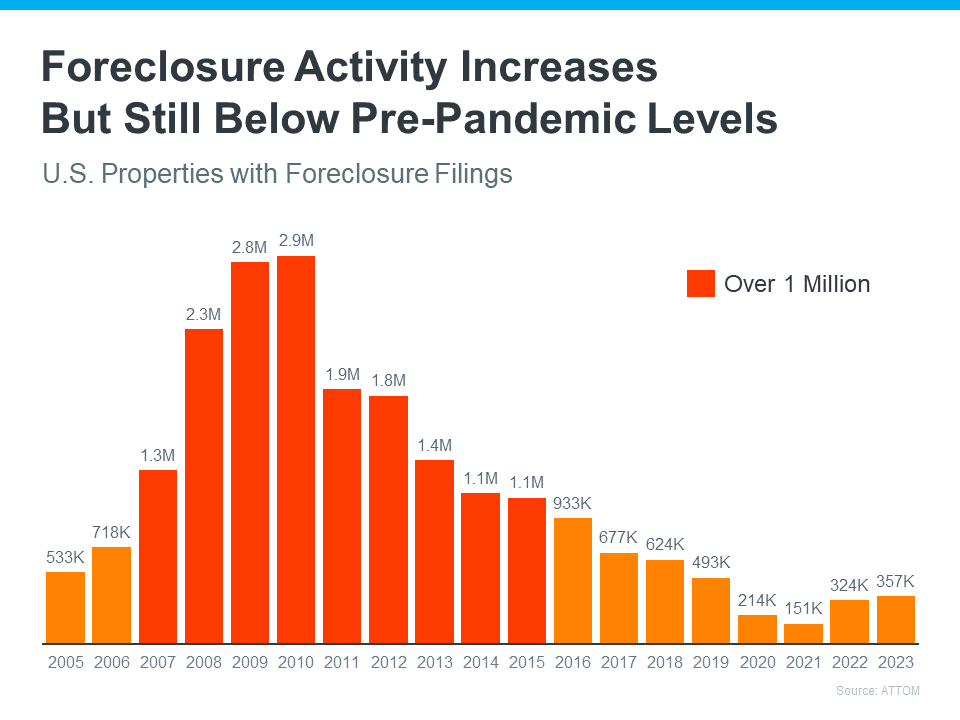

A broader historical perspective, stretching back to the 2008 crash, provides reassurance. Data from ATTOM, a property data provider, illustrates a consistent decline in foreclosure activity since the crash. Contrary to the fears of a repeat scenario, recent years have seen a significant decrease in foreclosure filings compared to the peak years post-2008.

One key factor distinguishing the current situation from the aftermath of the housing crash is homeowners’ equity. Unlike the widespread negative equity seen in the past, most homeowners today possess substantial equity in their homes. This equity acts as a buffer against foreclosure, contributing to the stability of the housing market.

In essence, the data paints a reassuring picture: there is no impending foreclosure crisis looming over the housing market.

In conclusion, it’s crucial to contextualize the data accurately. While foreclosures may be on the rise, they remain far from the crisis levels witnessed during the housing bubble burst. This increase is unlikely to precipitate a crash in home prices.